To Roth or not to Roth

Tax advantages for IRA conversions

A good financial advisor will use different tools available in order to blend your retirement income to minimize income taxes. Those tools may be distributions from a traditional IRA, dividends, or taking profits from brokerage accounts, pensions, and social security.

One of these tools, the Roth IRA, is getting a lot of attention lately because it may be used to minimize tax rates now and in the future. Many believe that tax rates are currently low and likely to be higher in the future. This means it may make sense to convert existing IRAs at today’s tax rates in order to be able to withdraw the money tax free in the future.

Roth IRAs and Taxes

Roth IRAs and Taxes

The IRS allows for immediate tax deferral for any funds you add to your traditional IRAs or 401(k) retirement accounts. The investments you make with these funds grow until you are eligible to withdraw them, and then it is taxed at the time that it is taken out of the account. These retirement accounts require minimum annual distributions every year after a certain age.

By comparison, Roth IRAs do not allow for current tax deferral. However, funds from Roth IRAs may be withdrawn tax free. Roth IRAs are also not subject to annual required minimum distributions, which makes them a great option for accumulating wealth for the next generation.

The IRS allows you to convert a traditional IRA into a Roth IRA. But how do you know when and if it would be best to convert some or all of your retirement accounts to a Roth?

The simple explanation is that if you anticipate higher taxes in retirement than the rate you pay now, a Roth conversion should be considered. While it’s impossible to know with certainty what rate you will pay in the future, many experts expect marginal tax brackets to increase above the historically low ones we are enjoying currently.

The Impact a Conversion Can Have

A partial or full conversion can offer tremendous benefits for your financial planning, but there’s a catch. The converted amount will be included in ordinary income, and could potentially impact other aspects of your planning, like the cost of your Medicare benefits. This means that there are some tricky calculations that need to be done in order to determine if this planning technique is right for you.

Here’s an example.

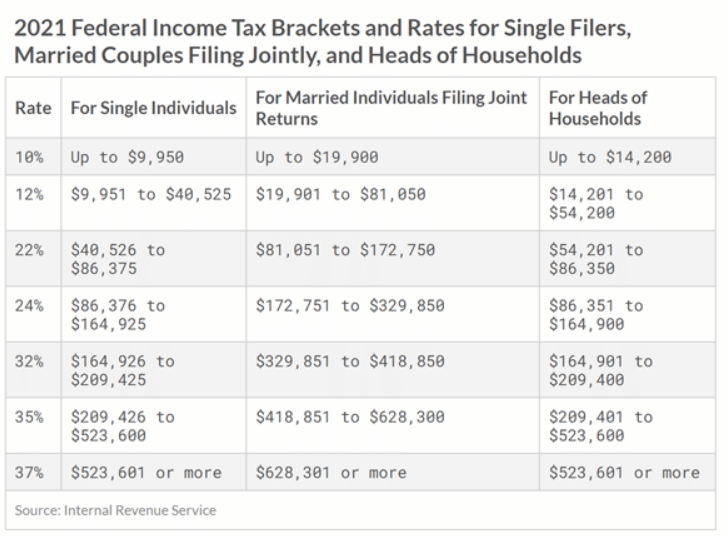

Bob and Edna Wyatt have a pension and rental income every year of $110,000. Based on the 2021 tax Bracket chart, they will pay a 22% tax rate. If they wanted to convert all or part of their IRA in 2021, they could pay taxes on and convert up to $62,750 to a Roth IRA their income would stay in the 22% tax bracket. Or they could decide to convert more. They know they will be moving into the 24% tax bracket the year they do the conversion. But it’s worth it to them because they want to avoid potential higher income taxes in the future and the Roth IRA, without minimum required distributions, will continue to grow tax free for their grandkids.

Let us help. Don’t be left behind. Learn if it makes sense for you to use this potentially powerful financial tool. Join our in-house financial advisor, Patrick Johnson, as he details the finer points of consideration for Roth Conversions.

Let us help. Don’t be left behind. Learn if it makes sense for you to use this potentially powerful financial tool. Join our in-house financial advisor, Patrick Johnson, as he details the finer points of consideration for Roth Conversions.

Click these links to read more:

SECURE Act: Stretch Inherited IRA Replaced with 10 Year Rule

Roth IRA Conversion Rules – Invinvestopedia

Protecting the Elderly From Financial Predators

We offer workshops and webinars every month for our clients.

A few of the workshops that address Roth IRAs process are:

Roth Conversions

You deserve an estate plan that changes with you. Choose a law firm committed to a lifetime of support and education for you and your family.

Author Bio

Catherine Hammond is the CEO and founder of Hammond Law Group, a Colorado-based estate planning law firm she founded in 2005. With a strong focus on protecting families from the legal consequences of disability and death, she creates comprehensive estate plans that minimize taxes, costs, and government interference.

A native of Denver, Catherine completed her undergraduate studies at Coe College in Iowa, and her Juris Doctorate from the University of Denver College of Law in 1993, concentrating on estate planning, tax, and mediation. Catherine is a member of various professional organizations, including WealthCounsel, ElderCounsel, the National Academy of Elder Law Attorneys, the Colorado Springs Estate Planning Council, and the Purposeful Planning Institute. Beyond her legal expertise, Catherine provides transformational coaching to support clients and their families through life transitions.

LinkedIn | State Bar Association | Avvo | Google