Taxes and Retirement – Plan Now to Save Thousands

Minimizing income tax and maximizing income in retirement

What are the best retirement vehicles for you, given your age, income bracket, tax bracket, and other factors?

A good financial advisor is much more than someone who gives you the best returns possible on your retirement investments. A good financial advisor will use different tools available in order to blend your retirement income to minimize income taxes. If you’re like many retirees, your retirement accounts are an important part of your retirement income. These may include IRA’s and 401k’s, dividends, or profits from brokerage accounts, pensions, and social security. Blending these investments and distributions from retirement accounts will help you stay in the lowest tax bracket in any given year, saving you significantly in taxes.

Very different tax approaches: Traditional vs ROTH accounts

Two different types of retirement accounts play very different roles in minimizing taxes in retirement. Traditional retirement accounts use tax-free investments to grow and require taxes be paid upon withdrawal during retirement. ROTH accounts are funded with after-tax earnings and may be distributed tax-free.

But which type of account is right for you?

Deciding between a traditional retirement account or a ROTH account is subtle and depends upon your long-term retirement income goals. One major consideration is your future tax rates. If it looks likely that you will be paying lower taxes after retirement, or if you still have a long time before retirement, ROTH accounts could be the best option.

Of course, it is impossible to know what tax rate you will pay in retirement. Many factors go into your tax rate, some of which are beyond your control. The US income taxes are historically low, suggesting to many that the rates will go up in the future helping them conclude that paying taxes now will be the cheaper option. These savers will choose the ROTH accounts and pay income tax now rather than later.

Aside from federal income tax rates, there are many things that might affect your taxes. Many retirees have paid off their houses and without a mortgage no longer qualify for a mortgage tax deduction, increasing their overall rate. But many retirees have less income and expenses in retirement, so they naturally pay lower taxes.

Converting Traditional Retirement Accounts to ROTH Accounts

In addition, the IRS allows you to convert your traditional retirement accounts to ROTH accounts, as long as you pay the taxes due prior to the conversion. Because these accounts are the main vehicle for retirement planning, many people have large enough accounts to see them through their retirement years. As such, converting all or even some of your traditional retirement accounts in any given year could bump your income into the highest marginal tax rates and result in a surprisingly high tax bill.

Understanding the Marginal vs Effective Tax Rates

One major concept that you must understand in order to determine whether a ROTH account or ROTH conversion is good for you is the concept of marginal tax rates vs effective tax rates.

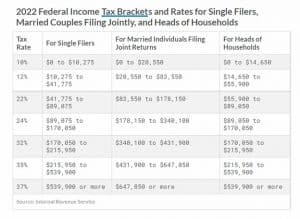

Income tax in the US is paid on a marginal rate. This means that different amounts of income are taxed at different amounts. Here is a copy of the 2022 tax bracket showing the seven different brackets. The goal with retirement income is to keep your income limited to the lowest bracket possible.

After your taxes are calculated for the year, you can calculate your effective tax rate. It is simply the total percentage of taxes you paid, divided by your income, in a percentage form. Your effective tax is helpful in retirement planning because it tells you the actual total taxes paid in any given year. You know if your income goes down, your effective tax rate will go down.

Decreasing Effective Rates by Planning with Marginal Rates

Your financial planner will consider all of your sources of income in any given year and modify distributions or sales of real estate or other investments in order to minimize your federal taxes. You might, for example, want to postpone the sale of a particular asset because selling it could put you into a higher marginal tax bracket. Selling this asset could be surprisingly expensive if it is counted as income, putting you in the highest bracket and requiring you to pay a 37% tax on the income from the sale.

The reason this is important for many retirees is that many have retirement accounts requiring minimum annual distributions after a certain age. These minimum distributions from traditional retirement accounts, counted as income, will set your minimum tax bracket, a sort of tax bracket floor for you in retirement.

The best way to lower your effective tax rates is to consider converting some of your traditional retirement accounts to ROTH accounts. Because ROTH account distributions are not considered income and do not require income taxes to be paid upon distribution, having more distributions from ROTH accounts can keep you from receiving income that would put you in the higher tax brackets, saving you significantly in taxes in any given year without decreasing distributions.

Learn more about ROTH Conversions

To Roth or Not to Roth Blog 2021

Does your retirement plan avoid these four risks?

A Comprehensive Guide to Tax Treatments of Roth IRA Distributions

Tax rates are key to deciding on traditional or Roth 401(k)/403(b)

Why Your Taxes In Retirement Will Likely Be Lower Than You Expect

Join us for monthly workshops and webinars to help you stay up to date on how to protect yourself and your loved ones during the most difficult times of life.

View upcoming Client Workshops.

Register for our Introductory Public Workshop, “The Essentials of Estate Planning.”

Author Bio

Catherine Hammond is the CEO and founder of Hammond Law Group, a Colorado-based estate planning law firm she founded in 2005. With a strong focus on protecting families from the legal consequences of disability and death, she creates comprehensive estate plans that minimize taxes, costs, and government interference.

A native of Denver, Catherine completed her undergraduate studies at Coe College in Iowa, and her Juris Doctorate from the University of Denver College of Law in 1993, concentrating on estate planning, tax, and mediation. Catherine is a member of various professional organizations, including WealthCounsel, ElderCounsel, the National Academy of Elder Law Attorneys, the Colorado Springs Estate Planning Council, and the Purposeful Planning Institute. Beyond her legal expertise, Catherine provides transformational coaching to support clients and their families through life transitions.

LinkedIn | State Bar Association | Avvo | Google